By Aleksandr V. Gevorkyan and Ingrid Harvold Kvangraven

Over the past decade, the Sub-Saharan African countries’ ability to draw on new debt in international capital markets has become a central characteristic of their development experience. Yet, the determinants of their borrowing costs are driven by external factors where investor perception plays a key role. This raises concerns over the sustainability of the current development model.

In the mid-2000s, 30 African countries received substantial debt reduction through the International Monetary Fund (IMF) and World Bank’s Heavily-Indebted Poor Country (HIPC) Initiative. Only a decade later, many of the same countries are again facing debt distress. The African Development Bank recently warned its members of the dangers of rising debt obligations, while the IMF has called for an “urgent need to reset” the region’s growth policies.

In our new paper entitled “Assessing Recent Determinants of Borrowing Costs in Sub-Saharan Africa” in the November 2016 issue of the Review of Development Economics, we trace the latest round of borrowing back to 2006 with Seychelles as the first sub-Saharan African (SSA) country to issue a sovereign bond, with the exception of South Africa, in 30 years. Since then, DR Congo, Gabon, Ghana, Côte d’Ivoire, Senegal, Angola, Nigeria, Tanzania, Namibia, Rwanda, Kenya, Ethiopia and Zambia have all followed suit, accumulating over $25 billion worth of bonds, with a principal amount of more than $35 billion (see Figure 1 for totals by country).

Figure 1. SSA Eurobonds by country for 2006-2016

Source: adapted from Gevorkyan and Kvangraven (2016)

Source: adapted from Gevorkyan and Kvangraven (2016)

As global investors search for yield, they are increasingly looking into emerging markets that borrow in foreign currencies (though few have been able to issue local currency denominated bonds). Barry Eichengreen has long argued, that the extent to which debt is foreign currency denominated, eventually becomes a key determinant of stability in output, capital flows, and exchange rate. For emerging markets such dynamics further exacerbate typical underdevelopment scenarios.

Similarly, Michael Pettis argues that the flow of international loans has been driven primarily by external events and not by domestic politics in developing countries since the 1820s. In that analysis, the flows of capital between rich and poor countries are generally determined by domestic conditions in rich countries, rather than the quality of investment opportunities in poor ones.

Recently, Gevorkyan and Canuto (here and here) have called attention to massive capital movements in and out of emerging markets and subsequent effects on macroeconomic development. The contradicting scenarios of financial deepening versus severe macroeconomic destabilization across smaller emerging economies are all too real. The new norm is low growth rates, continuous leveraging of global liquidity aided by low interest rates, and volatility in global markets.

Consistent with the above observations, our empirical results offer additional insights for a group of the SSA countries. We find that the yields on African sovereign bonds are closely correlated with the global capital markets’ volatility, changes in commodity prices and benchmarks for access to global liquidity. All three factors are outside of the developing countries’ control and in turn are highly influenced by investors’ perceptions of yet another set of three core factors: the health of the global economy, prospects of monetary tightening (or changes in monetary policy for that matter) in the developed countries, and the actual ability of the SSA borrowers to sustain interest payments as primary export commodity prices decline. “Perception” in this context is definitive and recent speculation on the US Fed’s actions seemed to have played, at least, a partial role.

As our paper predicts, many African countries are now facing repayment difficulties. Just two years after the Republic of Congo’s first bond issuance in 2007, Congolese bonds were trading for 20 cents on the dollar, pushing the yield to a record high. Seychelles received an IMF bailout at the height of the financial crisis in late 2008, and still has a soaring debt-to-GDP ratio.

Last year, Ghana had to enter an IMF bailout program with a range of austerity conditions. Ghana is in a difficult, yet unfortunately common, position as it depends on commodity exports such as gold, oil and cocoa, so with falling commodity prices, the country faces a decline in revenue and a growing current account deficit. Ghana’s total debt, both external and domestic, is now at more than 55% of its GDP.

The underlying problems

Why do African countries continue to run into debt difficulties? The answer lies in their lack of diversified economic structure and the resulting lack of real competitiveness on the international market. Running current account deficits, most of the SSA’s bond issuers have relied on external funding to make up for their trade balance.

Furthermore, the fundamentals of the sub-Saharan sovereign debt point to the commodities super-cycle upon which much of the past decade’s macroeconomic growth record is founded. And many SSA countries are heavily dependent on commodity exports, as per UNCTAD. Windfall revenues from commodity exports at the peak of the market have contributed to delayed action on structural changes, subduing the competitiveness problems across SSA and broader emerging markets, as Gevorkyan and Canuto argue. Such dependence on primary exports makes these exporter economies vulnerable to price swings and fluctuation in external demand.

In the context of export driven growth, structurally less diversified economies may be confronted with higher risks of default as foreign exchange revenues, needed to cover interest payments, depend on the export prices of just a few commodities. Commodity prices have been falling since 2013 and are projected to remain at low levels or even fall further in the near term.

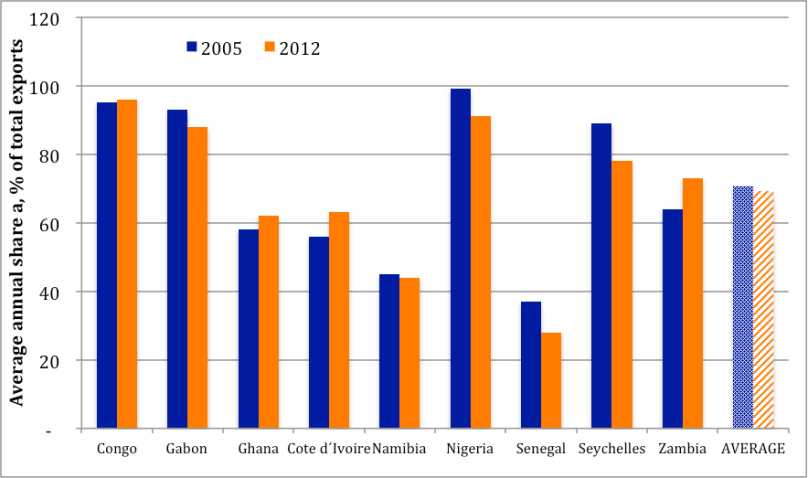

Figure 2 illustrates the severity of sub-Saharan African countries’ lack of diversification. According to an IMF definition, many SSA economies in our sample can be understood as non-diversified, i.e. where one sector accounts for up to 50 percent of total exports or where two sectors account for up to 80 percent of total exports, excluding manufacturing. The IMF characterizes the situation as a “shock of historic magnitude” facing the SSA primary exporter countries in the current declining phase of the commodity super-cycle.

Figure 2: Shares of the two largest export sectors as % of total exports

Source: authors’ calculation based on data from ITC (2014)

Source: authors’ calculation based on data from ITC (2014)

There is little that the SSA countries can do in the short run. Global financial volatility, a by-product of real demand and investors’ perceptions, drives much of price setting in primary commodities, with transmission shocks to the exporter countries’ terms of trade. And as Prebisch (1950) and Singer (1958) have long since argued, the subsequent terms of trade deterioration, leads to negative prospects of sustainable macroeconomic development. Elsewhere, Gevorkyan and Gevorkyan (2012) bring up over-dependence on primary commodity exports and derivatives volatility as destabilizing factors exacerbating already fragile macroeconomic conditions of the emerging exporter markets. Empirical evidence is abound, with Nigeria hitting recession in June for the first time in two decades following the collapse in oil export revenues and growing indebtedness, topped by domestic macro issues.

Considering that the underlying cause of SSA countries’ recurring debt crises is their lack of competitiveness, dependence on primary commodities, and non-diversified export base, to name a few, tackling the debt problem at its root would involve dealing with the abovementioned complex issues. As global financial volatility persists, the sub-Saharan African countries have more than domestic macroeconomic stabilization and fiscal consolidation problems to tackle.

Reference:

Gevorkyan, A. V. and Kvangraven, I. H. (2016), Assessing Recent Determinants of Borrowing Costs in Sub-Saharan Africa. Review of Development Economics, 20(4): 721–738. doi: 10.1111/rode.12195

Authors:

Aleksandr V. Gevorkyan is Assistant Professor of Economics at St. John’s University in New York City and a co-editor (with Otaviano Canuto) of Financial Deepening and Post-Crisis Development in Emerging Markets Current Perils and Future Dawns (Palgrave MacMillan, 2016). e: gevorkya@stjohns.edu

Ingrid Harvold Kvangraven is a PhD student in Economics at The New School for Social Research. She holds a Master’s degree in Development Studies from the London School of Economics. e: kvani263@newschool.edu

Originally published online by Interfima on October 10, 2016 http://www.interfima.org/publications/trouble-sub-saharan-african-debt/

Reblogged this on Radical Political Economy.

LikeLiked by 1 person

[…] The Trouble with Sub-Saharan African Debt (Developing Economics) […]

LikeLike