In his acclaimed poem “America” from 1956, Allen Ginsberg warned about the new vices of American society. Beyond the clear demonization of communist ideals, the star of the beat generation warned about the growing influence of the media on the thinking of individuals.

With globalization, the commodity fetishism disguised as the American dream entered not only the minds of the citizens of the United States but the rest of the globe. In addition, with the financialization of the economy, the debt culture also surpassed the American borders, reaching the countries of the Global South.

There is no day when the media does not bombard us with advertisements that promote a consumer culture, inciting us to acquire goods that we cannot afford with our income. This is where credit plays the role of a “savior entity” through which we can satisfy our deepest desires. However, unlike the developed countries, which have high levels of access to financial services, the underdeveloped countries are subject to a subordinated financialization that limits the possibilities of households and non-financial companies of acquiring a loan and, consequently, complicates the satisfaction of our consumerist spirit and the development of the productive sphere. The notion of subordinated financialization was first proposed by Jeff Powell (2013) to designate the specific way in which financialization manifests itself in underdeveloped economies. The level of access to financial services that a country has is known as financial inclusion, however, in the case of Mexico, this level is so low that we are facing financial exclusion.

Financial exclusion in Mexico

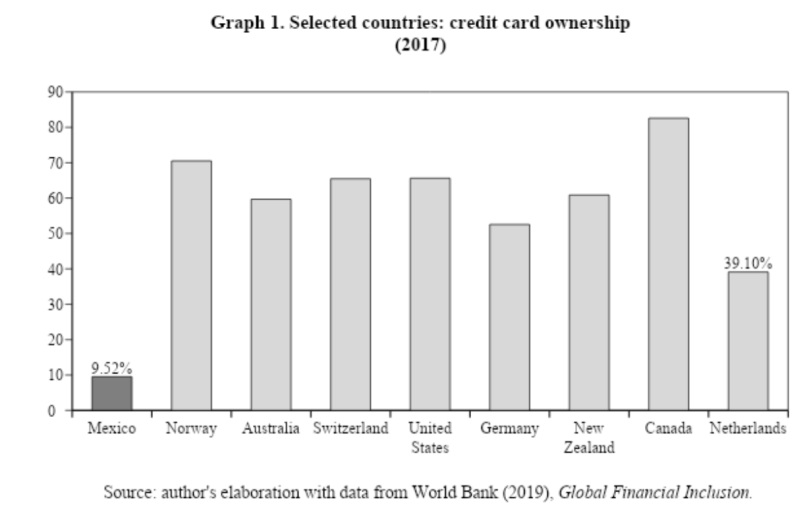

Let’s look at some basic data. In Graph 1 we can see the percentage of individuals who have a credit card in Mexico and eight developed countries. All the developed countries that appear in the graph had a percentage higher than 50%, except for the Netherlands, which had a proportion of 39.10%. However, this value is much higher than Mexico’s, which barely reached 9.52%.

What would be the cause of this exclusion? Taking a small step back, we can try to find the root of the problem in the modus operandi of the institutions responsible for lending to individuals: the banks. Focusing our attention on Mexico, let’s consider which banks are operating in this country.

Before moving on to the data and in order to delve a little into the new way of operating of the big banks in times of financialization, it is convenient to remember that, in 2011, when the Financial Stability Board published the first list of Global Systemically Important Financial Institutions (G-SIFIs), a select group of banks assumed the status of too big to fail and therefore, the perception of risk diminished for this select group of financial institutions.

The question now would be, can we talk about banks too big to fail in Mexico? Table 1 shows the composition of the Mexican banking sector, where the top 5 banks –BBVA Bancomer, Santander, Banamex, Banorte and HSBC– together reached 6,834,944 million Mexican pesos at the end of 2018, equivalent to 36.73% of that year’s GDP. The only national bank that appears on the list is Banorte which, in terms of its percentage of participation in the banking sector, 12.41%, is much smaller than the first bank on the list, BBVA Bancomer, which in 2018 represented the 22.05% of total bank assets. On the other hand, Santander’s parent company is in Spain. Banamex (recently renamed Citibanamex) is a subsidiary of Citigroup, the largest financial services company in the world, and the headquarters of HSBC is in the United Kingdom. The names of these four banks will seem familiar to us if we have looked at the most recent list of G-SIFIs, published by the Financial Stability Board in 2018. Indeed, the four main foreign banks that operate in Mexico form part of the select group of financial institutions too big to fail.

It is, therefore, necessary to ask ourselves, why the predominance of large banks in the Mexican banking system has not been reflected in a larger increase in access to financial services. Banks operating in Mexico impose restrictions when granting credit so that only people who prove to have a medium or high monthly income are granted a loan. It’s well known that banks tend to not lend to low-income individuals to reduce the risk of default in the case of a recession, but what risk? Are they not supposed to be too big to fail? One explanation could be that being immune to risk, banks that are too big to fail are more concerned with participating in complex financial operations than by increasing their credit portfolio to citizens. This new business model of banks, in which its income became more dependent on commissions for the purchase and sale of securities, and part of its profitability comes from shadow banking operations, involves higher risks than traditional lending.

To wrap up, banks too big to fail have a strong presence in the Mexican banking sector. However, the participation of foreign banks has failed to promote financial inclusion to an adequate degree, given that Mexico’s population still has a low level of access to financial services. It therefore becomes clear that subordinate financialization involves not only the lack of funding of non-financial companies but also the financial exclusion of individuals.

References

Financial Stability Board (2011), Policy Measures to Address Systemically Important Financial Institutions.

Financial Stability Board (2018), 2018 list of global systemically important banks (G-SIBs).

Powell, Jeff (2013), Subordinate financialisation: a study of Mexico and its nonfinancial corporations. PhD Thesis. SOAS, University of London.

Giovanni Villavicencio has a degree in Economics from the Universidad Nacional Autónoma de México. @giomvill.