Developed countries often lecture developing and emerging countries on the appropriate policies and institutions necessary for economic success. This is done either bilaterally or through multilateral organizations such as the World Bank, IMF, OECD or European Union. Cambridge economist Ha-Joon Chang exposed the hypocrisy of this approach in his provocative 2002 book Kicking Away the Ladder: Development Strategy in Historical Perspective. Chang suggests that when today’s rich countries were themselves developing, they used practices opposite to what they preach today, including industrial policies, high tariffs and infant industry protection. Therefore their current advice to poorer countries amounts to ‘kicking away the ladder’ of development.

A lesser-known but equally disturbing process has occurred in the realm of economic statistics, in particular national income accounts. The EU and OECD often criticize the national accounts of developing countries, and a recent example is a claim made in a blog by Robert Barro: “There are suspicions that China’s reported growth rates in recent decades have been boosted by manipulation of the national-accounts data.” While no statistical system is beyond doubt, the biggest manipulations of data in history, in fact, have benefited (and were supported by) rich countries.

The Rhetoric of Economic Statistics

Efforts to measure the ‘economy’ have taken place since the 17th century, beginning with William Petty’s Verbum Sapienti (1665) and Political Arithmetick (1676). Right from the beginning, this seemingly technical exercise has involved geopolitical competition to establish the economic (and by extension, military) superiority of countries. William Petty and Gregory King in England, as well as Pierre de Boisguilbert and Marshall Vauban in France, all used their estimates of national income to demonstrate their countries’ fiscal strength (or weakness) and urge for certain policies (for a political history of this practice see Gross Domestic Power: Geopolitical Economy and the History of National Accounts).

A recent parallel of this statistical race was the revision of US GDP (for 2013 Q2) by the Bureau of Economic Analysis (BEA). The new definition used by the BEA includes R&D and original entertainment works in fixed investment, whereas these were previously classified as intermediate inputs and thus excluded. This revision added $560 billion to total US GDP (more than the whole economy of Sweden), increasing it to $16.2 trillion, and conveniently “reinforcing America’s status as the world’s largest economy and opening up a bit more breathing space over fast-closing China” (Economist Intelligence Unit, 2013). Canada had done the same in 2012 and Australia as early as 2009, “leapfrogging Canada in the OECD’s country rankings of GDP per person” (The Economist, April 3, 2013).

These statistical maneuvers pale, however, in comparison to the 1968 revision to the international standard called the System of National Accounts (SNA). Up to this point, the interest income of banks (traditionally derived from financial intermediation) had been completely left out of the national accounts, as it was considered merely an unproductive transfer. The 1968 SNA “made finance productive” (Christophers, 2011) by a bizarre sleight of hand, which presented net interest earned by banks as an input to a ‘notional’ (read: imaginary) industry. This strange treatment was given the name Financial Intermediation Services Indirectly Measured (FISIM), to distinguish it from financial fees, which were directly measurable.

The Financialization of GDP

While this revision gave finance a foothold in GDP (and made the output of other sectors paying this interest seem lower), it did not affect the overall level of GDP. And at that point in time, the other stream of financial income – explicit fees charged by banks and other financial institutions – was relatively small. In time, however, the share of finance, insurance and real estate (the FIRE sectors which create and trade assets rather than produce and sell goods and services) rose dramatically in a process called Financialization, and financial fees increased accordingly. In 1997, the last year in which the US reported FISIM separately (afterwards it was ‘distributed’ to uses, meaning deducted from other sectors’ net outputs), net interest income was just 3.1% of GDP, while the fee-based profits (‘value-added’) of the FIRE sector accounted for 27.1% of GDP. By 2011 (the last year for which sectoral data are available), fee-based FIRE ‘output’ (in reality imputed based on net income) accounted for a staggering 33% of total US value added (or 36% of GDP).

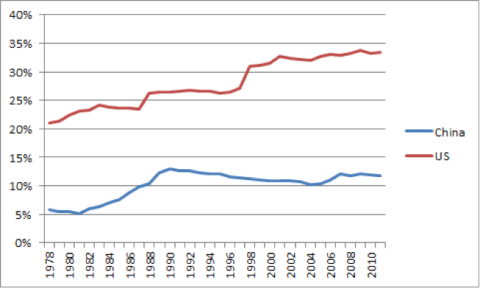

What does all this have to do with developing countries? Both financialization and therefore the financial sector’s statistical footprint in GDP are much larger in developed countries than in developing ones. In China, for example, although the FIRE sector doubled its share of GDP from 6% in 1978 to 12% of GDP in 2011, it still only accounts for less than an eighth of all economic activity. In the US, by contrast, the FIRE sector has gone up from over a quarter (26.5%) of GDP in 1990 to over a third in 2011 (see figure 1).

Figure 1: FIRE sectors as share of GDP, China and US

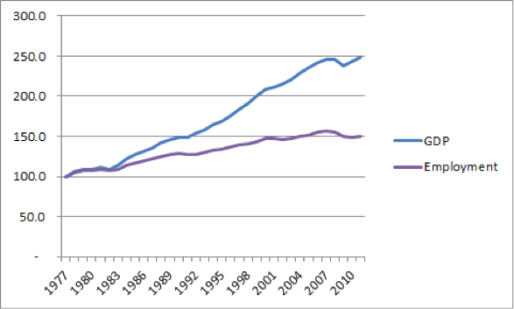

Recent research has suggested that the imputation of productive output for the FIRE sector in the national accounts has distorted GDP in several ways. First, the FIRE imputation drives a wedge between output (as measured by GDP and employment trends), as visible in the phenomenon of ‘jobless growth’ observed after the three most recent recessions in the US (see figure 2).

Figure 2: US GDP (constant prices) and total employment, 1977=100

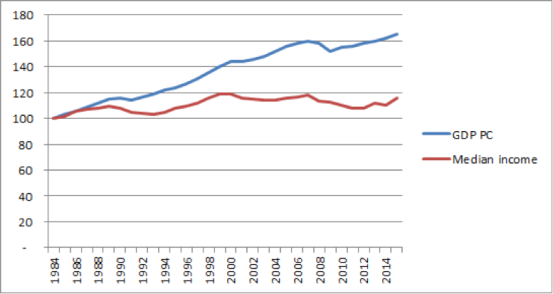

Second, real per capita GDP has likewise diverged from a more realistic measure of standard of living, real median income. This divergence of overall economic growth from an experience of stagnation for the median voter has been at the heart of increased inequality, and has also been cited as one of the reasons for the rise of populism in the recent US election (e.g. the Sanders and Trump movements) and perhaps also Brexit in the UK.

Figure 3: US per capita GDP (constant prices) and median income, 1984=100

Putting out the FIRE

These and other anomalies have been investigated by recent research, which has also proposed some corrected measures of output. Basu and Foley (2013), in their paper Dynamics of output and employment in the US economy, exclude the FIRE sector from their measure of output (called Non-financial Value Added or NFVA) and find a much improved correlation between NFVA and GDP. In my own research, I go a step further, first excluding and then deducting financial fees from GDP. This is symmetrical to the treatment of financial interest income (FISIM) in the SNA, and also echoes Nordhaus and Tobin’s treatment of some government services as ‘instrumental’, i.e. intermediate consumption. I call this adjusted measure Final GDP (FGDP), since it treats finance as an intermediate input to the rest of the (productive) economy, and deducts it as such (for a full discussion of this methodology and its implications for economic theory and policy, see my new book on the Financialization of GDP).

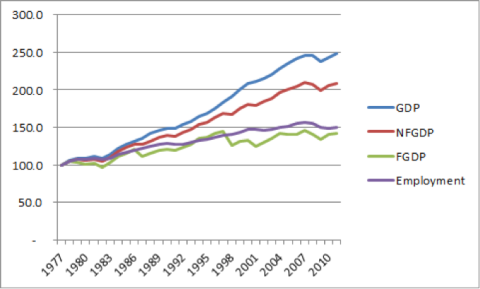

Figure 4 shows GDP against FGDP and NFGDP (the GDP equivalent of Basu and Foley’s NFVA). Both alternative measures match employment better than GDP, with FGDP being the closest. FGDP also fits median income far better than per capita GDP, and even performs better than GDP in forecasting employment trends (see this working paper).

Figure 4: Three measures of US output (constant prices) and employment, 1977=100

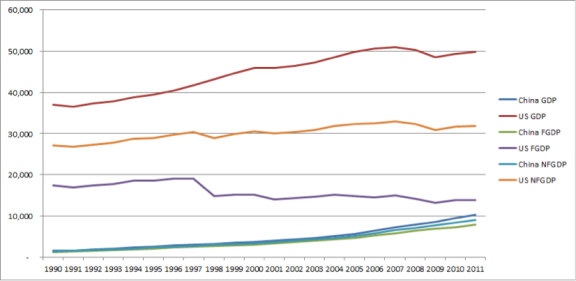

What would FGDP imply for a developing economy like China? Given the small and relatively stagnant size of its financial sector (compared to the US, UK etc.), one would expect the distortion to GDP (and its concomitant correction in FGDP) to be smaller than that for the US. Figure 5 illustrates that this is indeed the case. While per capita FGDP and NFGDP are lower than GDP per capita (as they both exclude finance and FGDP further deducts it from GDP), the differences are not dramatic (China’s real per capita income in $PPP increased by over 500% by all measures). Furthermore, comparing the three measures across the two countries gives us a new insight into the extent of convergence between them.

Figure 5: Per Capita measures of output, PPP (constant 2011 international $)

As mentioned, China’s three measures are pretty close to each other given the relatively small share of FIRE in its economy. In the US, on the other hand, official GDP per capita (in 2011 $PPP) increased from $37,062 in 1990 to $49,782 in 2011, an increase of 34%. Just excluding FIRE, NFGDP per capita starts from a lower $27,224 in 1990 and rises less dramatically to $31,841 in 2011, a 17% increase. FGDP, by contrast, actually declines by 20%, from $17,387 in 1990 to $13,901. This implies, for the US, that while financial activity (and net revenues) exploded in the past two decades, the real US economy (net of financial fees) has stagnated and even contracted. More importantly for the present discussion, China has caught up far more than previously thought if we consider FIRE as a cost or economic input rather than impute to it an artificial ‘output’. Per capita GDP would have us believe that in 2011 China’s income per head was only 21% of that in the US. NFGDP presents it as 28%, but FGDP, by ‘putting out the FIRE’, so to speak, shows Chinese per capita income to be a more realistic 56% of American GDP.

Measuring Development in Historical Context

Going back to Barro’s claim that Chinese GDP statistics are manipulated, this last chart seems to suggest that rich countries have gone even farther. Advanced countries (which influenced the revisions to the SNA in 1993 and 2008 through the EU, OCED, World Bank and IMF) have portrayed themselves as more productive and richer based on imputations of output to the FIRE sectors, which merely create and trade assets rather than goods and services. This amounts to kicking away the statistical ladder, by moving the goalpost for developing countries by defining growth differently now from when the US and others were industrializing (i.e. employment-intensive production in agriculture, manufacturing, utilities and non-financial services).

The national accounts treat the two income streams of the FIRE sectors inconsistently, since they deduct net interest income from GDP as an input to other industries but add financial fees income to GDP as ‘value added’. There is no conceptual reason for this (it is simply easier to capture fees than it is interest differentials). If we correct this inconsistency by deducting both interest and fee incomes of the FIRE sector from GDP (as ‘instrumental expenditures’ in Nordhaus and Tobin’s term), we not only solve a conceptual problem and improve the performance of our measure of output vis-a-vis employment and median income trends, but we also judge developing countries’ progress by the same yardstick afforded to more advanced ones when they were at the same level of development.

Dr. Jacob Assa is Economic Affairs Officer at the United Nations. The views expressed herein are those of the author and do not necessarily reflect the view of the United Nations.

Data: UNData and World Bank WDI

Photo: William Murphy

[…] Kicking Away the (Statistical) Ladder (Jacob Assa, United Nations) […]

LikeLike

[…] in development economics – on this blog (for example by Adel Daoud, Ingrid H. Kvangraven, or Jacob Assa) and elsewhere (for example by Angus Deaton, Dani Rodrik, and Benjamin Selwyn), as well as in […]

LikeLike