By Aleksandr V. Gevorkyan (St. John’s University) and Tarron Khemraj (New College of Florida)

In May 2016, economist Kenneth Rogoff argued that central banks in emerging markets should add gold to their reserves. Rogoff stated “that a shift in emerging markets toward accumulating gold would help the international financial system function more smoothly and benefit everyone.” Despite initial disagreement, we find there may actually be some justification for this view in a recent paper coming out in Emerging Markets Finance and Trade.

Until recently, literature on the optimal composition of foreign exchange reserves could be divided into two groups. The first focused on demand for reserves for transaction purposes (Soesmanto et al. 2015, Eichengreen and Mathieson 2000, Dooley et al. 1989, Heller and Knight 1978). The second, using a Markowitz-type portfolio approach, studied currency composition of optimal foreign reserves (Ben-Bassat 1980, Papaioannou et al. 2006, Ito et al. 2015). On a more general level, some studies offer more comprehensive discussion of factors determining the optimal level of international reserves (e.g. Bahmani-Oskooee and Brown, 2002; Aizenman and Lee, 2007).

Instead, we develop an analytical model that allows for estimation of the shadow price of the target exchange rate, which is interpreted as the central bank’s sacrifice of policy precision given additional unit of portfolio variance or return.

This means that while we explicitly assume that central banks in emerging (and frontier) markets target exchange rate stability, there may also be competing pressure to maximize portfolio returns based on the international reserves mix.

To be sure, gold is not a new asset to central banks’ portfolio, neither historically, nor recently (Fig 1.). However, there has been a steady decline in gold holdings as central banks shifted towards a hard currency (e.g. U.S. Treasuries) mix of reserves. The low income and middle income economies have lowest shares with minor increases in the post-2008 years.

Figure 1. Percent of gold in central banks’ foreign reserves by country group.

Source: authors’ estimations based on data from the IFS (2017) and WDI (2017).

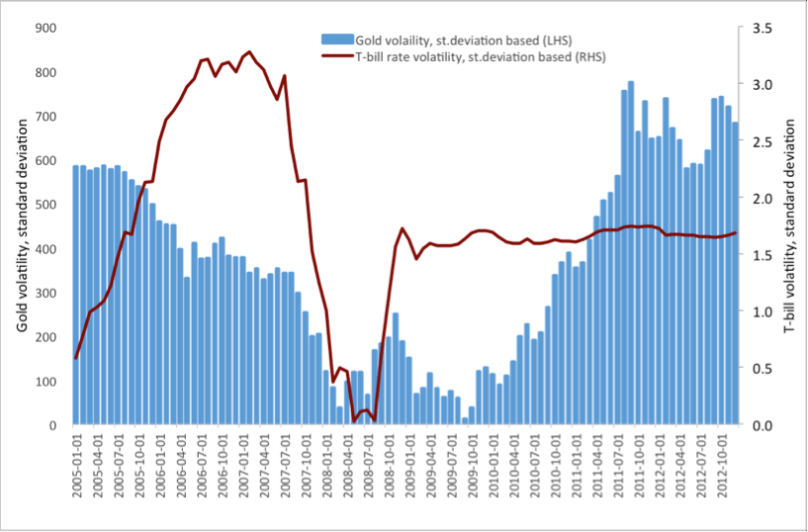

In the years before the 2008 Global Financial Crisis (GFC) both volatility of gold and U.S. Treasuries declined (Fig. 2). Gold dropped off first, rising momentarily, and then stabilizing. U.S. Treasuries followed, but on balance both assets may be seen as safe havens given their lower volatility during the GFC.

Figure 2. Estimated volatility of gold and U.S. Treasuries, 2005 to 2012

Source: authors’ estimations based on data from FRED (2017).

In a simulated local economy in our paper, there may be range of preferences (and perceptions) towards currency depreciation (or policy devaluation) and appreciation, expressed by θ_1 and θ_2 respectively, given the central bank’s holdings of foreign reserves relative to the policy target. In many small open economies θ_1 would tend to be greater than θ_2 reflecting the higher aversion to devaluation. At the same time Π is the foreign exchange market’s expected subjective or calculated short-run probability of depreciation or devaluation.

The central bank’s exchange rate target – that requires foreign reserves balancing – is constrained by (i) the volatility introduced by adding gold to the portfolio of reserves; and (ii) a weighted reaction function that combines both portfolio variance and return. Some central banks might also want to manage foreign exchange reserves subject to returns (e.g. Pina, 2017).

The central bank is assumed to react negatively to volatility and positively to returns. In the model this is captured by Ψ which takes values between 0 and 1. If Ψ =1, then the monetary authority is completely in the corner of the precautionary motive as it targets the exchange rate. On the other hand, if Ψ =0 the central bank is completely focused on returns as it pursues the exchange rate target.

As such, we construct a model capturing domestic foreign exchange market, adding gold demand constraint and analyzing the policy sacrifice shares in two regimes. The first, which we define as precautionary case, focuses on maintaining a currency target rule. The second, which we define as a hybrid case, adds central bank’s considerations for both portfolio variance and returns.

A representative central bank seeks to choose a level of gold that minimizes the loss function subject to portfolio volatility and some combination of volatility and returns. In other words, we want to choose a percent share of gold WG when the policy sacrifice (λ) is at a minimum when takes values from 0 to 100%.

We are also interested in whether the range of values increases or decreases sharply or gradually. If the sacrifice value is increasing or decreasing slowly, one could conclude that it is possible to demand gold over the said range without significantly preventing the central bank from achieving its exchange rate target.

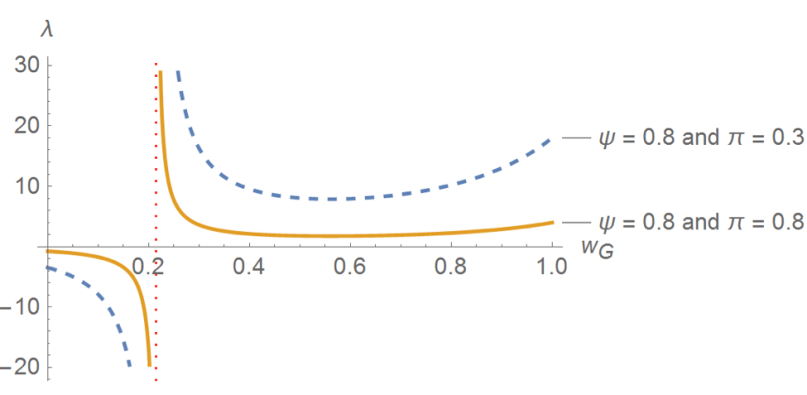

Our simulations (Fig.3 reports example of the Hybrid Case) indicate possible existence of a two-regime demand for gold. In policy terms multiple equilibria suggest the monetary authority possibly has a wide percentage range of gold demand.

Figure 3. Hybrid Case: returns and volatility constraint for Ψ =0.8

In Figure 3 the weight reflecting the central bank’s preference for precaution is higher at Ψ =0.8. The sacrifice values on the vertical axis are smaller. The conclusion here is that if the central bank is motivated by the precautionary motive, then an exchange rate target could be consistent with about 45 to 60 percent gold reserves in the portfolio without significant loss of policy sacrifice, assuming that the economy possesses the given parameters. In the hybrid case, a higher probability of devaluation causes the curve to shift downward and expand the range of possible gold percentages. This suggests that central banks have a range of gold shares to opt for with somewhat minimal sacrifice in exchange rate target policy precisions.

The overall conclusions suggest there is some justification to the original view of adding gold to the central bank’s reserves in emerging and frontier markets. Demanding a higher percentage of gold is more appropriate if the central bank prefers to accumulate international reserves for precautionary reason. At the same time, the central bank would tend to incur greater exchange rate target sacrifice if it wants to achieve higher portfolio returns. Our estimations suggest that ability to target the exchange rate is unaffected by the higher volatility of monthly returns on gold. That in turn suggests that gold might be replaced with another safe asset with similar characteristics.

The latter observation, opens up a much greater range of monetary policy flexibility to the countries susceptible to externalities from global capital flows and lacking strength in the domestic currency.

References:

Aizenman, J. and J. Lee (2007) “International reserves: precautionary versus mercantilist views, theory and evidence.” Open Economies Review, 18 (2), 191 – 214.

Bahmani-Oskooee, M. and F. Brown (2002) “Demand for international reserves: a review article.” Applied Economics, 34 (10), 1209 – 1226.

Benn-Bassat, A. (1980) “The optimal composition of foreign exchange reserves.” Journal of International Economics, 10, 285 – 295.

Eichengreen, B. and D. Mathieson (2000) “The currency composition of foreign exchange reserves: retrospect and prospect.” IMF Working Paper No. 131, International Monetary Fund.

Dooley, M., J. S. Lizondo and D. Mathieson (1989) “The currency composition of foreign exchange reserves.” IMF Staff Paper, 36 (2), 385 – 434.

FRED (2017) FRED Economic Data. Online Database. St. Louis, MO: Federal Reserve Bank of St. Louis. Available online: https://research.stlouisfed.org

Gevorkyan, A.V. and T. Khemraj. Forthcoming. Exchange rate targeting and gold demand by central banks: modeling international reserves composition. Emerging Markets Finance and Trade.

Heller, H. R. and M. Knight (1978) “Reserve currency preferences of central banks.” Essays in International Finance, No. 131, Princeton University.

IFS (2017) International Financial Statistics. Online database. Washington, D.C.: International Monetary Fund. Available online: http://www.imf.org/en/Data

Ito, H., R. McCauley and T. Chan (2015) “Currency composition of reserves, trade invoicing and currency movements.” Emerging Markets Review, 25, 16 – 29.

Papaioannou, E., R. Portes and G. Siourounis (2006) “Optimal currency shares in international reserves: the impact of the euro and the prospects for the dollar.” Journal of Japanese and International Economies, 20, 508 – 457.

Pina, G. (2017) “International reserves and global interest rates.” Journal of International Money and Finance, 74, 371 – 385.

Rogoff, K. (2016) “Emerging markets should go for the gold.” Project Syndicate, May 3.

Soesmanto, T., E. Selvanathan and S. Selvanathan (2015) “Analysis of the management of currency composition of foreign exchange reserves in Australia.” Economic Analysis and Policy, 47, 82 – 89.

WDI (2017) Word Development Indicators. Online database. Washington, D.C.: World Bank. Available online: http://databank.worldbank.org/

Aleksandr V. Gevorkyan is Assistant Professor of Economics at St. John’s University and Tarron Khemraj is Associate Professor of New College of Florida.