Official calls are mounting. On March 23, African Finance Ministers met virtually to discuss their efforts on the social and economic impacts of COVID-19. Amidst a broad recognition of chronic financing gaps to meet development and climate objectives, they called for a moratorium on all debt interest payments, including the potential for principal payments for fragile states. The United Nations General Secretary addressed the G20 emergency meeting conference call on COVID-19. Along with calls for medical and protective equipment, the need to prioritise debt restructuring was stressed, “including immediate waivers on interest payments for 2020”. The World Bank President addressed the emergency G20 Finance Ministers encouraging bilateral IDA relief without missing the opportunity to plug for structural reforms.

The G20 statement replete with grand aspirations, but no timeframe specified to fulfil them, was vague in respect to debt issues and far short of what is needed: “We will continue to address risks of debt vulnerabilities in low-income countries due to the pandemic.” Hardly commensurate to the alarm bells that have been ringing loudly and repeatedly over the past five years of growing debt difficulties in a number of countries.

On March 25th, the IMF and World Bank issued a joint call for an immediate suspension of bilateral debt payments for countries eligible for concessionary IDA facilities. They called “on all official bilateral creditors to suspend debt payments from IDA countries that request forbearance”. On the same day, Ecuador’s Congress called on government to suspend debt payments to all lenders to free up resources needed for addressing the pandemic. Meanwhile, Ethiopia’s Prime Minister, on March 25th, discussed the disastrous frequency with which debt service payments pile higher than those of annual health budgets. UNCTAD, with a longstanding critical eye on debt issues had already released an update for its flagship report on Trade and Development that called for a moratorium from the 9th March. On the 30th March, UNCTAD called for an immediate debt standstill on sovereign debt payments, followed by significant debt relief to the amount of $1 trillion this year, to be overseen by an independently created body.

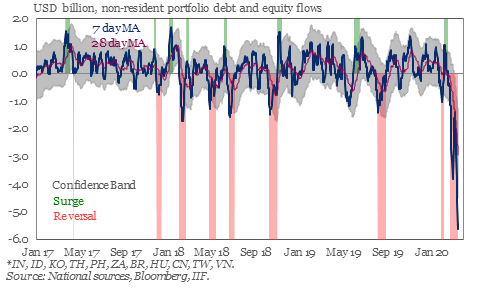

For IDA countries, the savings of a moratorium would be substantial. According to Eurodad, US$15.4 billion in 2020 are currently tied to official external bilateral loans, which would rise by 3.8 billion if multilateral institutions are included and $5.9 billion including external private creditors – a total of 25.5 billion for 2020. In developing countries with higher incomes, the last two months have seen close to $80 billion fly out, “more than three times the amount of cross-border outflows in three months after the outbreak of the global financial crisis in September 2008”, according to the Institute of International Finance, and “the largest capital outflow ever recorded” according to IMF.

Figure 1: Daily non-resident portfolio flows to a subset of emerging markets (USD billion)

Source: IIF

The sudden stops and reversals of capital flows currently occurring as global liquidity tightens brings upon significant problems: currency depreciations pose problems for monetary policy and dollar denominated debts. These, however, build upon and amplify longstanding structural issues: an increasing share of borrowing from private lenders and the lack of international lender of last resort.

There are few palatable or available options.

Decades of decimation of public health care at the behest of IMF conditionality has led to underfunded care systems in low income economies. Close to 50 low income countries spend more resources on public debt service than on health care systems: average 7.8% as a share of GDP on debt service as compared to 1.8% on public health services. Reducing public health budgets, cutting public funding to make quick short-term economic savings have been to the detriment of long-term health benefits. Yet development finance under the rubric of the Addis Agenda has sought to address dwindling public budgets through the involvement of the private sector in the delivery of key development goals.

Financing facilities of multilateral agencies traditionally have a disastrous reliance on conditionality. Calls for new issuances in SDRs, the reserve assets of the IMF, have been made but large increases, as the one after the global financial crisis, need amendments to the IMF’s mandate. Similarly, access to the Fed’s dollar swap lines was widened on March 19th to include a broader group of countries such as Mexico and Brazil, and the attempt to ease dollar shortage furthered on March 31st allowing any central bank with an account at the New York Fed to use their foreign exchange reserves (US treasury securities) as collateral for low interest dollar loans. But can this suffice for all?

Given the immediate response to the pandemic has been unilateral and uncoordinated, reaffirmed by generic promises on the G20 level, it is worth bringing to the fore some options. A recent call was made for capital controls in order to immediately “curtail the surge in outflows, to reduce illiquidity driven by sell-offs in DECs’ markets, and to arrest declines in currency and asset prices”.

The debt moratoria called for, supported by several civil society organisations (for instance: Jubilee Debt Campaign, Eurodad, Jubilee USA, German jubilee network), would be more relieving if they included debt repayments due to multilaterals, as they are significant creditors for low income countries. Although it has been argued otherwise, moratoria would fall short if only for officially provided loans: private creditors are a growing and significant aspect of external credit for low income countries, as they have been for some time, a fact highly related to conditions of global liquidity. Any benefits that accrue from suspending bilateral payments may be reaped by private creditors, as has been done repeatedly, so excluding them would be a dubious use of public funds. The multi-pronged approach proposed by UNCTAD encompasses these elements and amounts to what should have been delivered to developing countries over the past decade had the DAC of the OECD met their 0.7% ODA target.

For too long, debtor countries deal with such problems in a fragmented, incoherent and unfair way, facing numerous overlapping jurisdictions and creditor procedures. For bilateral debt, the Paris Club has been repeatedly shunned for lacking legitimacy; and for multilaterals, the eligibility criteria are subject to heavy conditionality. Repayment difficulties to private creditors are hounded by the rise of litigation, usually in countries where the creditors are based. Calls for better and more equitable ways to deal with debt repayment difficulties of low and middle incomes in an institutional setting such as the UN has been tried several times. In fact, developing countries have been putting the issue on the table since 1964 but it has been repeatedly blocked by creditor countries.

Free public health care, prevention of mass evictions, social protection for those in the informal sector, self-employed and those least able to cope with the pandemic were among the messages made on March 20th by Juan Pablo Bohoslavsky, the UN Independent Expert on the effects of foreign debt and human rights. “No private economic entitlement should trump public’s rights to health and survival”. If debt relief is at the same time used to push more loans and structural reforms, in a context of humanitarian health emergency, the human right to health imperative must prevail over debt service rigidity.

Christina Laskaridis is a PhD candidate in Economics at SOAS, University of London, and co-convenes the Politics of Economics seminar series at the University of Cambridge and the Ceteris Never Paribus podcast. She tweets at @ChristinaLaska1.

Fully agree, see also http://www.ipsnews.net/2020/04/covid-19-jolt-g20-collective-action/

LikeLike

[…] an almost exclusive control of the world market of health.” Neocolonial debt further hinders Global South public health by diverting already limited state resources away from funding health care systems to servicing […]

LikeLike

[…] is constrained by these external factors, activists, academics, and policy-makers have called for debt moratoria, IMF support, and debt relief as necessary […]

LikeLike

[…] of health systems in many African countries, but also to understand the political economy of the contemporary debt and capital flight crises unfolding on the continent in the wake of the […]

LikeLike