By Jan Fichtner and Johannes Petry

In the past, during the time of the “Washington Consensus” developing countries from the Global South faced the IMF and the World Bank as their main counterparts in important matters of global finance. Based on our recently published research paper “Steering Capital” we argue that due to an ongoing paradigm shift in financial markets this constellation is changing profoundly. A new breed of Wall Street firms is emerging that occupies a pivotal position in the relationship between (developing) countries and financial markets – index providers.

This rise of index providers is grounded in the global shift towards passive investment. Formerly, investors gave their money to funds where a well-paid fund manager was picking stocks (or bonds) with the aim to produce above average returns – to “beat” the market in finance parlance. But now more and more investors invest in cheap passive funds (which comprise both exchange traded funds and index mutual funds) that merely track financial indices. Unlike actively managed funds, however, the passive index funds industry is characterised by enormous economies of scale – in terms of technology it is not a big difference if a passive fund has ten million or ten billion US$ assets under management. In addition, there is a strong first mover advantage. As a result, BlackRock, Vanguard and State Street dominate passive funds as the “Big Three”. Excellent recent work has since focused on how this “new money trust” is shaping the emergent ”American Asset Manager Capitalism”.

What is not yet adequately discussed is the fact that these asset managers effectively delegate their investment decisions to a small group of index providers, which own, construct and maintain the key global benchmark indices. Global stock indices are dominated by S&P Dow Jones indices, MSCI and FTSE Russell. In fixed income (i.e. bonds) Bloomberg has played a huge role ever since it bought the widely tracked Global Aggregate Bond Index suite from Barclays in 2016. While especially for countries in the Global South, JPMorgan is another important index provider as it owns the important Emerging Markets Bond Index.[1]

As ever more assets track the equity and bond indices by this new burgeoning group of “passive” Wall Street firms we need to research what this means for states in the Global South. Is the growing influence of index providers in this era of passive investing leading to a new kind of financial subordination and uneven financialization of developing countries in Africa, Asia and Latin America, perpetuating the structural hierarchies that characterise global financial markets?

One finding is that in developing countries in which index funds hold a larger share of the stock market cross-border financial flows are more sensitive to financial conditions in the Global North. Moreover, when countries (or firms) are downgraded or excluded from widely tracked indices, all the passive funds that replicate the index are forced to sell these assets. The result is quasi-automatic financial outflows from the particular country. This mechanism arguably puts pressure on developing countries to take index methodologies into account in their financial regulatory frameworks. Conversely, the prospect of being upgraded or included into key indices constitutes an accolade for many countries as it signifies the trust of the global investment community and causes financial inflows worth billions of US$. MSCI’s inclusion of China A-shares is estimated to result in US$400 billion of capital inflows over the coming years. The decisions of index providers increasingly move markets – especially for more volatile investments into emerging markets.

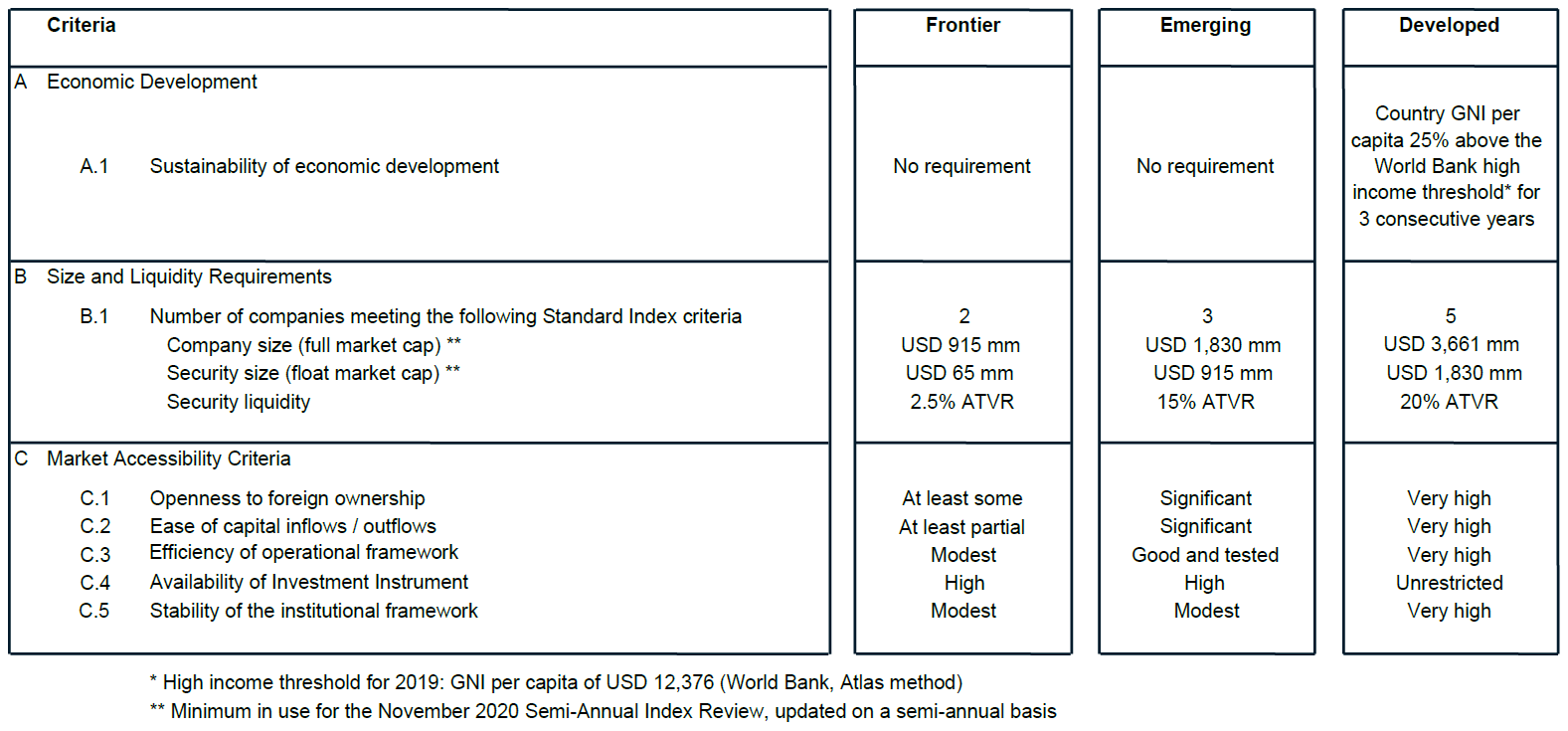

In the first political economy article on index providers we investigate how index providers determine capital flows into (and out of) countries. The figure below shows the MSCI Market Classification Framework. We argue that the primary criterion and the one that is most likely to influence developing countries is “market accessibility”, which includes openness to foreign ownership and ease of capital in- and outflows. The criteria “economic development” and “size and liquidity requirements” are not crucial and relatively easy to fulfil. What matters when it comes to “steering capital” are index providers’ evaluations of a countries’ foreign investment regimes.

Source: MSCI Index Methodology

These assessments of market accessibility, however, are based on qualitative measures that MSCI (and other index providers) reviews for all markets at least once a year during its Global Market Accessibility Review. This approach provides MSCI with a high degree of discretion and ”ample space for subjective judgement on whether certain countries should be considered frontier or emerging markets.” This matters a lot. While the MSCI Emerging Markets index serves as a benchmark[2] for assets under management worth US$1.8 trillion, its frontier market index is tracked by only US$14 billion. A reclassification therefore has enormous consequences for countries . In the words of the Financial Times, “MSCI […] in effect controls the definition of which countries are ‘emerging markets’”. As the dominant global provider of emerging markets indices, MSCI has emerged as a crucial counterpart for developing countries.

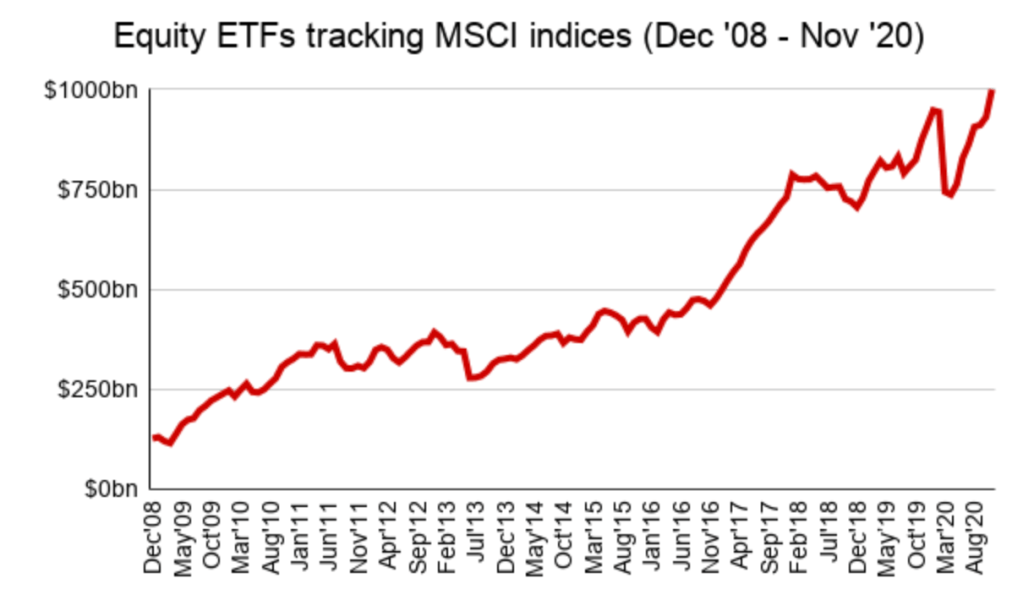

The ongoing avalanche of capital into passive funds supercharges the influence of the major index providers. As one of our interviewees puts it: “the big index providers, they are setting standards! […] Before, nobody paid attention, but now so much money follows them, […] they have a lot of political power!” In fact, in November 2020 the assets of equity exchange traded funds that directly track MSCI indices have surged past the US$1000 billion milestone for the first time while funds worth US$14.8 trillion use MSCI’s indices as benchmarks.

A few examples highlight the growing clout of index providers. In 2015 the finance minister of Peru, accompanied by staff from the central bank, reportedly hurried to New York. The purpose was neither to go to the United Nations nor to meet the IMF or the World Bank. Instead, the reason was that rumors were circulating that the large index provider MSCI would relegate Peru from its widely tracked MSCI Emerging Markets Index to the lower Frontier Markets Index. The mere fact that MSCI thought about downgrading Peru from emerging to frontier market status resulted in a 5% drop of the Peruvian stock market. Peru managed to avert this relegation by changing financial market regulations, easing global investor access and engaging in “roadshows with institutional investors” but this episode shows for states from the Global South the actions of index providers are highly consequential.

Similarly, JPMorgan removed Nigeria from its Emerging Markets Bond Index in 2015 because the country had implemented currency controls which hindered market accessibility. In mid-2020, MSCI put Argentina and Turkey on its “watchlist” for possible exclusion from its Emerging Markets Index as market accessibility deteriorated substantially in both countries. In the case of Turkey, this is expected to trigger about $5bn in total outflows from Turkish equities, including about US$2-3 billion from passive investment funds that automatically track the index. Instead of international financial institutions such as the IMF or World Bank, these episodes illustrate that in the new era of passive investing, index providers have become key gatekeepers in global finance.

It has recently been argued that we witness the metamorphosis of the “Washington Consensus” into the “Wall Street Consensus” which can be defined as an “elaborate effort to reorganize development interventions around selling development finance to the market.” The major index providers will play a key role in this new era of global finance. Even though the funds that track this index ecosystem are called “passive”, the firms that own and construct the dominant financial indices exert a growing active influence on states – especially on developing countries in the Global South.

Jan Fichtner is a Senior Research Fellow at the CORPNET project, University of Amsterdam.

Johannes Petry is an IRC Postdoctoral Research Fellow at the SCRIPTS Centre of Excellence, Free University of Berlin. @johannes_petry.

Photo: MSCI

NOTES

[1] JPMorgan is the last big bank that owns an important suite of indices. The Wall Street giant also trades emerging markets bonds. Due to this potential conflict of interests and increasing regulation of index provision (e.g. the European Benchmark Regulation) it seems likely that JP Morgan will eventually sell its indices. MSCI would be the natural buyer as it owns the dominant emerging markets equity indices.

[2] Index funds fully replicate the specific index they track, while most actively managed funds have one index to which they compare (or “benchmark”) their performance and from which they thus are not able to diverge substantially.

Photo by Unsplash/Markus Spiske

[…] [developingeconomics.org’daki orijinalinden Pelin Tuştaş tarafından PolitikYol için çevrilmiştir.] […]

LikeLike

[…] in the developed North, it continues to deepen extraction in the Global South, both actively and passively. Moreover, the global corporate takeover by big tech is not devoid of the footprint of digital […]

LikeLike

[…] in the developed North, it continues to deepen extraction in the Global South, both actively and passively. Moreover, the global corporate takeover by big tech is not devoid of the footprint of digital […]

LikeLike